Solid Q4 Results From Liquidia

Details from Q4 release and call for Liquidia

Liquidia (disclosure: long - see full disclaimer) did pre-announce their Q4 topline numbers, so there was less incremental news with the Q4 release. Nonetheless, management hit the following points, all broadly positive and confirming of the thesis that the stock has momentum and appears undervalued:

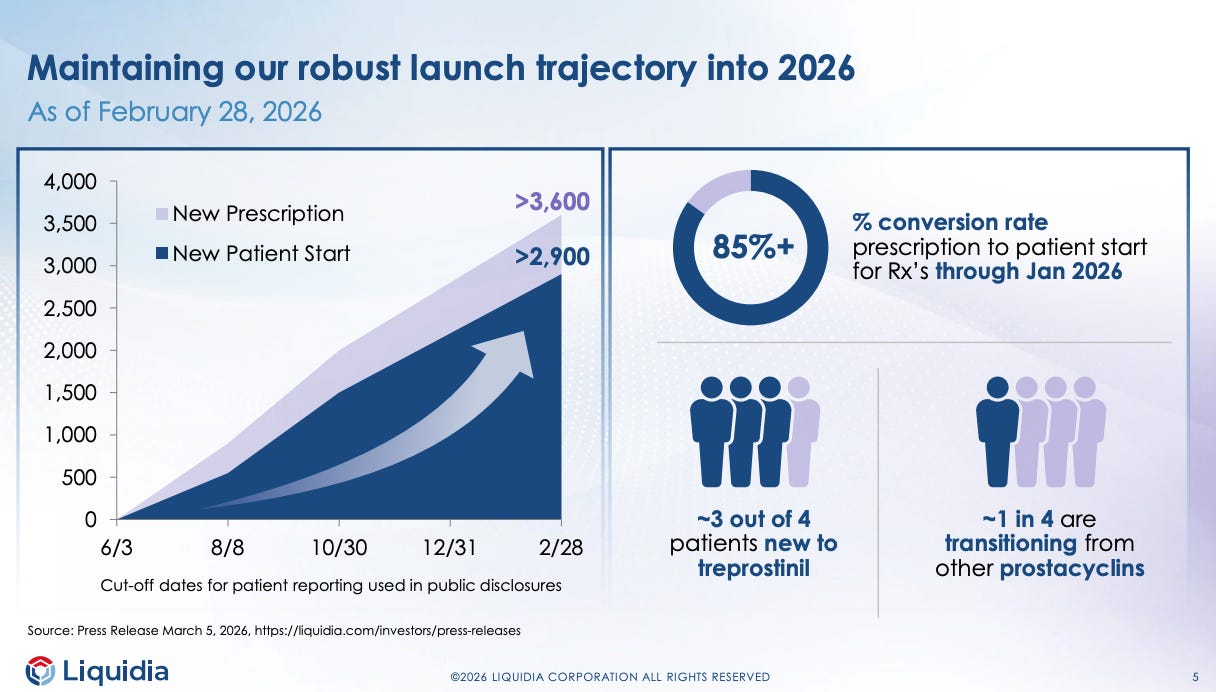

Shared patient start data to end Feb 26 that suggested a similar rate of growth as seen in Q4 (see slide below). Said “exact same trajectory” [as Q4] in response to question.

Continue to expect over $1B in revenue in 2027 (vs. $148M of revenue in 2025 with a June launch). CFO said “on our path to be a billion dollar product in 2027”.

Were clear that they see share gains relative to United Therapeutics (this was evident in sales figures, but interesting to hear a previously less aggressive management team verbalize it). Specifically, they described 25% of patients as “transitioning from other prostacyclins” per slide above.

They also took some time on the call (via response to question) so explain why United Therapeutics recently mentioned Soft Mist Inhaler might not be a compelling product. Yes, it may be more portable, but without changes to particle size (as Yutrepia has via PRINT) you still may get significant cough and won’t reach lower airway. The Chief Medical Officer at Liquidia was of the opinion that SMI inhalers haven’t been shown to offer any improved clinical efficacy beyond portability.

Looking to launch trials for Yutrepia for systemic sclerosis (rare condition) later in the year.

No new news on the legal case, expect a decision soon (just as they did in December and January!), remain optimistic.

Summary Valuation and Conclusion

To check in on valuation, $1B sales in 2027, which is starting to look a little conservative suggests $600M of free cash flow as compared to a current market cap of $2.8B, so sub 5x 2027 free cash flow on management ‘guidance’.

Why is $1B in 2027 conservative? Well, if they can add an absolute

+7% points of share a quarter (as they appear to be doing) and the market grows +5% sequentially each quarter (as it seems to be doing), then they may hit $1B run-rate by Q1 2027, and even hit ~$860M of revenue for full-year 2026.

The main risk currently is an unfavorable legal ruling (maybe a 20% chance) and that the competitive landscape may change with upcoming product launches in 2027-8, but Liquidia’s L606 product appears well-positioned there.

Disclaimer

The content on this site is provided for informational and educational purposes only and is not intended as investment advice, financial advice, or a recommendation to buy or sell any security. The views and opinions expressed herein are solely those of the author and do not constitute professional investment guidance.

No Duty to Update: This content reflects the author’s opinion as of the date of publication and may contain inaccuracies, errors, or misstatements. The author assumes no obligation to update, correct, or revise this content for any reason, including changes in market conditions, company circumstances, or the discovery of errors.

Professional Advice Required: Before making any investment decision, you should consult with qualified financial, investment, and tax professionals who understand your specific financial situation, investment objectives, and risk tolerance. Tax implications of options trading can be complex and vary based on individual circumstances.

Risk of Loss: All investing involves risk, including the possible loss of principal. Options trading may result in losses exceeding your initial investment in certain circumstances. Only invest capital that you can afford to lose entirely, and ensure any investment aligns with your financial goals, time horizon, and risk tolerance.

No Guarantees: Past performance is not indicative of future results. No representation is being made that any account will or is likely to achieve profits or losses similar to those discussed in this article.

Not an Offer or Solicitation: Nothing on this site constitutes an offer to sell, a solicitation of an offer to buy, or a recommendation regarding any security, investment product, or trading strategy.

No Client Relationship: Use of this site does not create a fiduciary, advisory, or client relationship between you and the author. The author is not acting as your investment adviser and has no obligation to act in your best interest.

Data and Third-Party Sources: Any data, charts, quotes, or other information may be obtained from third-party sources believed to be reliable, but their accuracy and completeness cannot be guaranteed. The author is not responsible for any errors, omissions, or delays in such information.

Forward-Looking Statements: Certain statements may be forward-looking and inherently uncertain. Actual results may differ materially from those expressed or implied. The author undertakes no obligation to update any forward-looking statements.

No Liability: The author and the site assume no liability for any losses, damages, or expenses arising out of any use of this content, including but not limited to trading losses, market losses, or any actions taken based on the information provided.

Affiliations and Disclosures: The author may hold positions in the securities mentioned and may change such positions at any time without notice. Any such holdings do not constitute a recommendation and should not be relied upon as investment guidance.